They say if you go “woke,” you go broke, and plenty of companies have learned that lesson the hard way in recent years.

Consumers on both sides of the aisle have turned against brands they feel betrayed them. (Personally, I was more upset about Jaguar’s redesign. It looks like my dream car will have to be an Aston Martin instead.)

That’s why Cracker Barrel (Nasdaq: CBRL) has been in the spotlight lately. Its latest rebrand was painted as going “woke” – which nowadays almost seems to mean making any change at all. Then, just days later, management walked much of it back.

While the media obsessed over the culture war angle, investors were left with a simpler question: Is there money to be made in this stock?

Let’s get to the meat and potatoes.

For the uninitiated, Cracker Barrel is a roadside staple of southern comfort, serving meatloaf, biscuits, and fried chicken alongside country-themed retail. It operates about 660 restaurants across 43 states, plus the smaller Maple Street Biscuit Company chain.

The company has faced a rough patch in recent years, and management was forced to slash its once-generous dividend from $1.30 per quarter to $0.25.

Revenue for the most recent quarter came in at $821 million, up just 0.5% from the prior year. Restaurant sales rose 1%, thanks largely to menu price hikes of nearly 5%. But the retail side of the business struggled, falling 3.8%.

Earnings improved year over year, with net income swinging to $12.6 million, or $0.56 per share, versus a loss of $9.2 million or $0.41 per share last year. Adjusted EBITDA (earnings before interest, taxes, depreciation, and amortization) was essentially flat at $48.1 million, a razor-thin 0.4% increase.

Management did raise full-year adjusted EBITDA guidance to $215 million to $225 million, showing some confidence in its turnaround efforts. But at the same time, capital expenditures remain heavy ($160 million to $170 million), and wage and commodity inflation continue to bite.

Now let’s strip away the distracting headlines and see what The Value Meter says.

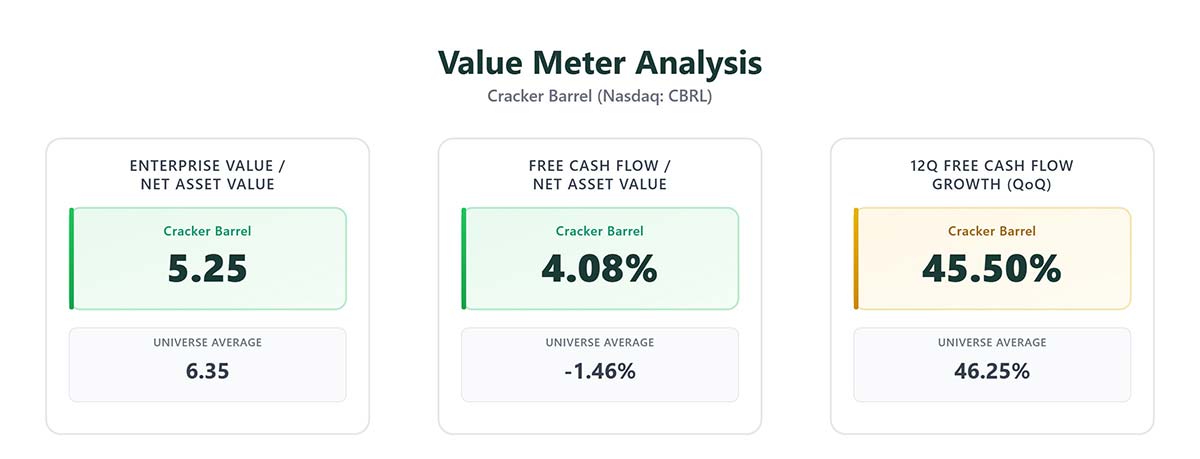

Cracker Barrel has an FCF/NAV ratio of 4.08%, compared with a universe average of -1.46%. That means it is more efficient than the typical company at converting its net assets into cash. Positive cash generation in a tough industry counts as a win.

Additionally, Cracker Barrel’s EV/NAV ratio stands at 5.25, while the universe average is 6.35. Put simply, investors are paying less for each dollar of net assets than they would for the average company. That tilts the value picture in Cracker Barrel’s favor.

However, the company’s cash generation is spotty. Over the last three years, Cracker Barrel grew its free cash flow quarter over quarter 45.5% of the time – nearly identical to the market average of 46.25%. That shows stability, but not outperformance. Cash flow is positive, but not reliably growing.

In short, Cracker Barrel isn’t broken, but it isn’t booming either.

It’s generating a bit more cash than the average company relative to its assets, and it trades at a discount in terms of EV/NAV. But its growth consistency is only average, and the business still faces headwinds from inflation and consumer belt-tightening.

Meanwhile, the stock has been on a roller coaster. After trading above $75 in late 2023, shares sank below $40 by late 2024 as traffic slowed and investors worried about the dividend cut.

But from that low, the stock staged a strong rebound, climbing back over $64 before, again, falling to about $35. Now, shares seem to have settled around $62.

The swings reflect a market that’s still undecided on whether the turnaround has real staying power.

Investors shouldn’t expect a screaming bargain here – nor should they expect a disaster. Cracker Barrel looks to be priced about right for what it is: a steady but challenged operator in a tough industry.

The rocking chairs on each restaurant’s front porch may be built for lingering, but the stock doesn’t give investors much reason to do the same.

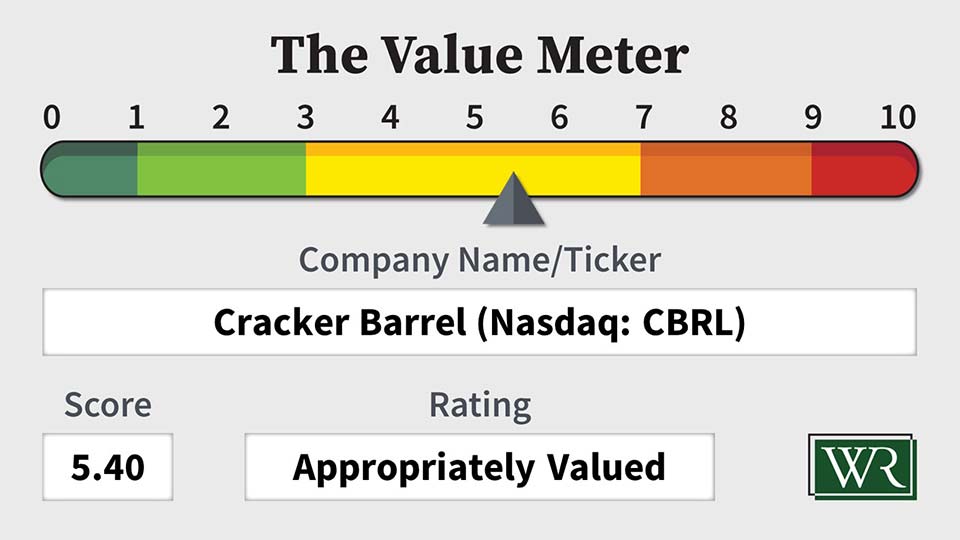

The Value Meter rates Cracker Barrel as “Appropriately Valued.”

What stock would you like me to run through The Value Meter next? Post the ticker symbol(s) in the comments section below.

The post What’s Really Cooking at Cracker Barrel? appeared first on Wealthy Retirement.